Editorial SeregaSibTravel/iStock via Getty Images

presentation

As a dividend growth investor, I sometimes revisit the companies I sell. I sell companies when they cut their dividends. I try to create a logic to return to investments that have failed me. Sometimes me too they regain shares in companies that have cut their dividends. It was the case of Kinder Morgan (KMI).

One stock I held in the past was Carnival Cruise (NYSE: CCL). Carnival Cruise suffered tremendously from the pandemic, as it forced the company to shut down all of its operations for more than a year. I sold my shares as soon as the dividend was eliminated. Therefore, I avoided most of the share price decline that followed as investors realized the gravity of the situation. In this article, I’ll revisit the company to see if it’s worthy of patient dividend growth investors with a long investment horizon.

I will analyze the company using my methodology for analyzing dividend growth stocks. I am using the same method to make it easier to compare researched companies. I will review the company’s fundamentals, valuation, growth opportunities and risks. Then I’ll try to determine if it’s a good investment.

Alpha Company summary search shows that:

Carnival Corporation operates as a leisure travel company. Its ships visit approximately 700 ports under the brand names Carnival Cruise Line, Princess Cruises, Holland America Line, P&O Cruises, Seabourn, Costa Cruises, AIDA Cruises, P&O Cruises and Cunard. The company also offers port destinations and other services, and owns and operates hotels, lodges, glass dome railways and buses.

Grounds

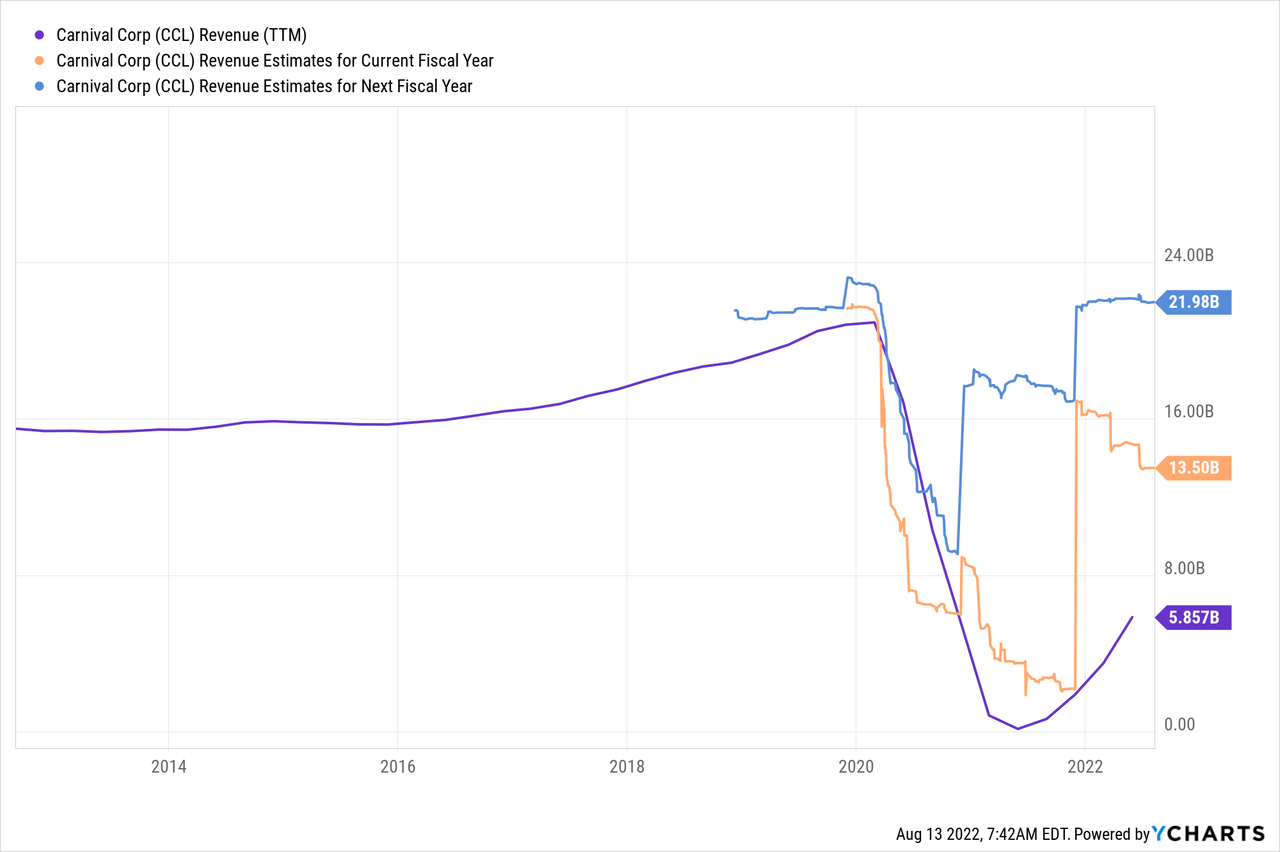

Carnival Cruise enjoyed steady sales growth until the pandemic in 2020. 2019 was a record year for the company and the first time Carnival Cruise surpassed $20 billion in revenue. The pandemic has destroyed their growth plans and sales were close to zero for four consecutive quarters. However, we see a recovery in sales in 2022, after the company released its second quarter report, which showed a 50% increase in sales compared to the first quarter. According to analyst consensus, as seen in Seeking Alpha, the company is expected to more than double sales in 2022, and in 2023 the company should reach an all-time high in revenue.

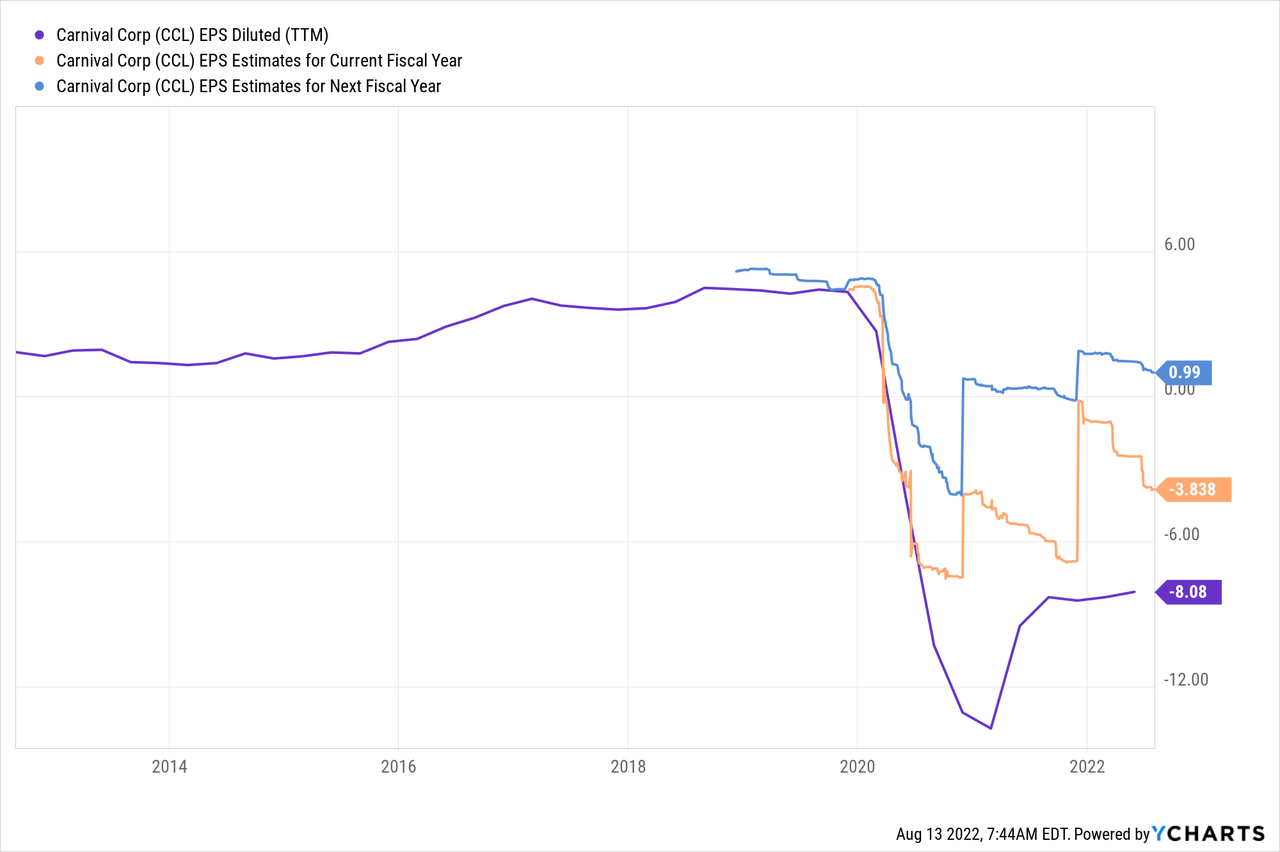

EPS (earnings per share) is a more challenging metric for Carnival Cruise. The company has lost billions of dollars and had to take on debt to stay afloat. Expenses have increased, and so has the number of shares outstanding. Hence, the 2019 EPS recovery will take longer than 2023. However, investors may see the light in the second quarter as the company continued to lose money, but cash from operations finally turned positive. According to analyst consensus, as seen in Seeking Alpha, the company is projected to reduce its losses in 2022, and in 2023 the company should achieve full-year profitability with an EPS of $1.

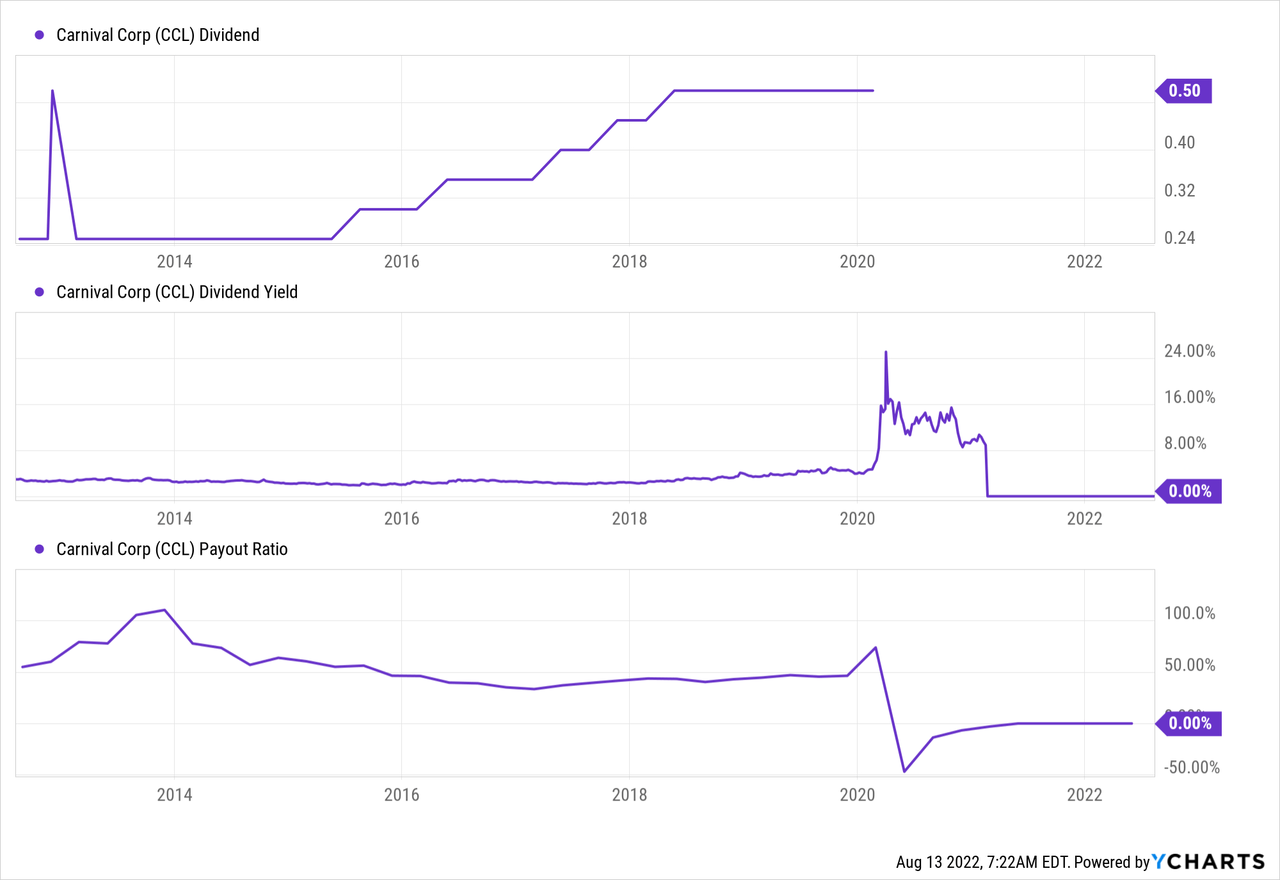

The company was paying dividends to its shareholders reliably. It cut distribution in 2008 during the financial crisis, but has since adopted a more conservative policy. However, no policy could sustain the dividend during the pandemic when the dividend was much higher than sales. Therefore, the dividend was eliminated and will be reinstated only after the company stabilizes and devalues its balance sheet as debt serves as an operational risk.

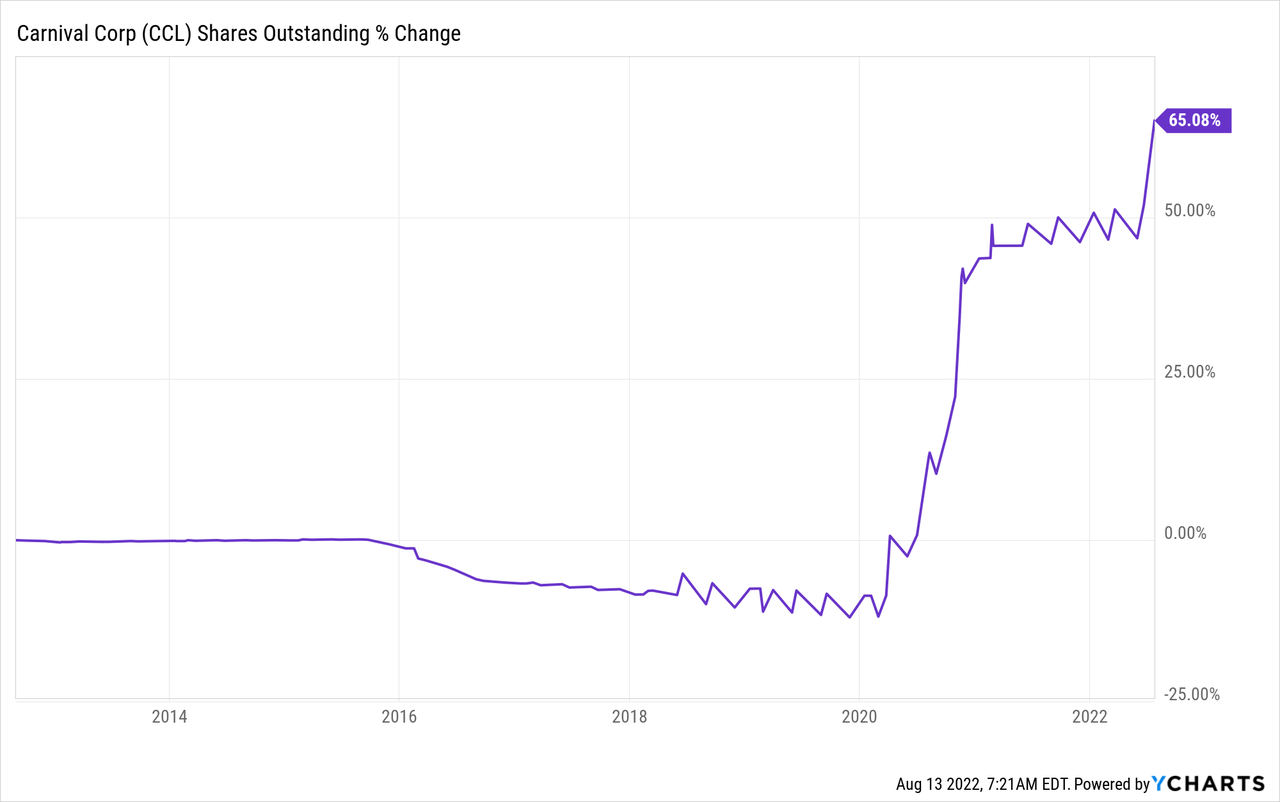

In addition to dividends, companies tend to return capital to shareholders through buybacks. Repurchases support future EPS growth, thereby allowing for faster dividend growth and more capital return. Carnival Cruise has been diluting its shareholders with aggressive stock issuance as the company was forced to raise cash to survive. This dilution means it will be harder to recover EPS as there are many more shares outstanding.

ASSESSMENT

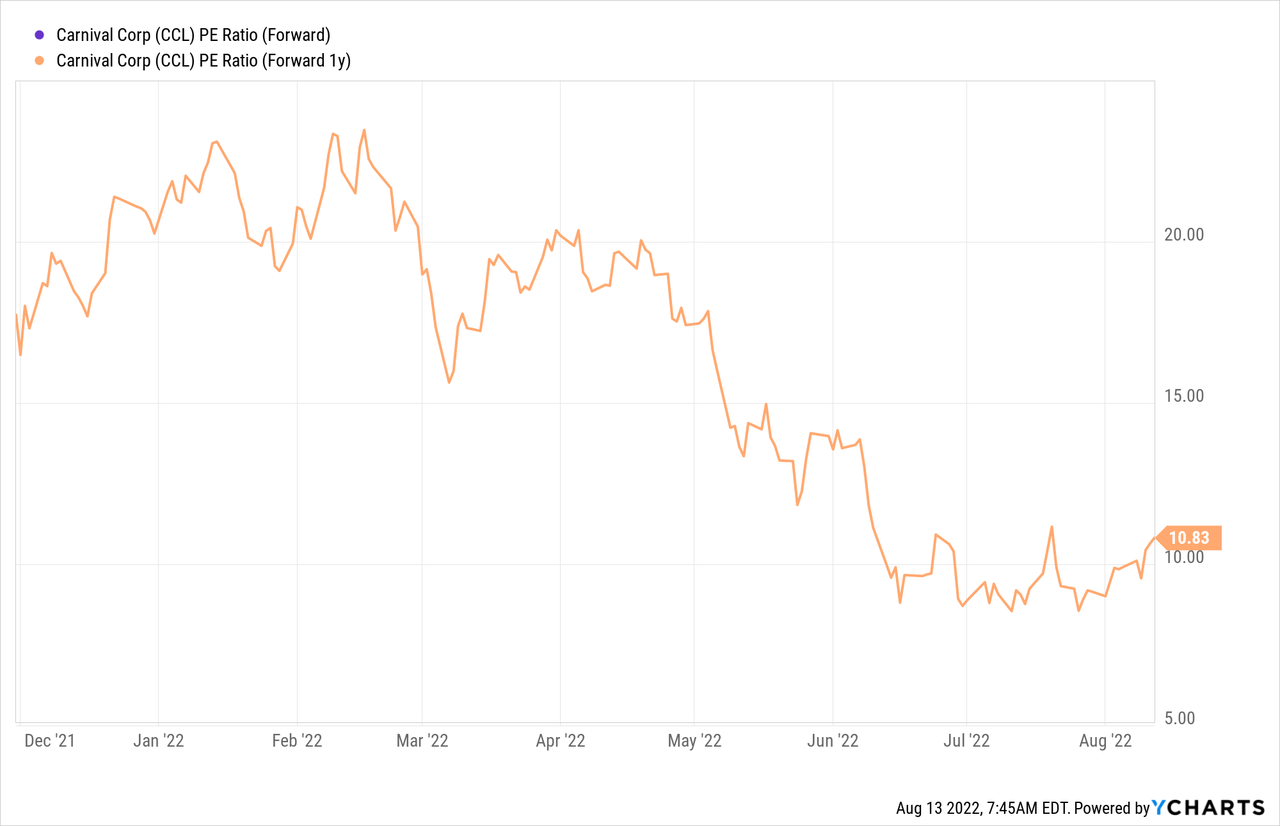

The P/E (price to earnings) ratio is tricky to analyze for Carnival Cruise’s valuation. The reason for this is that the company is still losing money. However, when looking at projected EPS for the fiscal year ending November 2023, less than 18 months away, the valuation looks attractive as the company is trading for less than 11 times forward earnings. It is much nicer than it was just a few months ago.

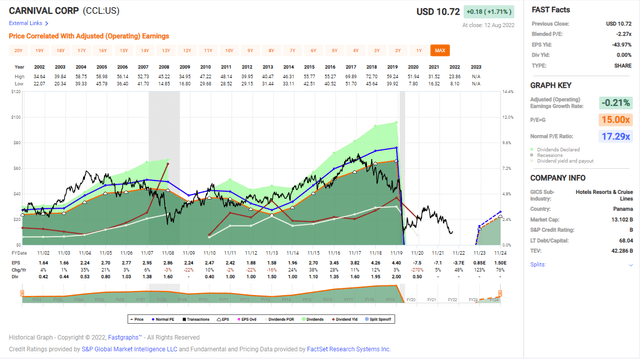

The chart below from FAST Graphs also highlights that in terms of valuation, Carnival Cruise is attractive. The average company valuation in the last twenty years was about 17, and until the pandemic, the company grew by 6% per year. For now, investors can take advantage of the company’s projected faster growth along with its depressed current valuation, which is significantly lower than average.

FAST Charts

To conclude, Carnival Cruise has weak fundamentals. Due to the pandemic, its sales and EPS reset, it carries much more debt and stopped paying dividends. Moreover, it issued more shares, so the recovery in 2019 will take longer. However, the company offers an attractive valuation that could attract long-term patient investors. The company looks like a long-term play on its ability to recover and return to normalcy.

OppORTuNiTy

The most important growth opportunity is for the world to return to normality. We see metrics improve for Carnival Cruise as people have enough confidence to book cruises. Sales are growing by double digits quarter after quarter, cash from operations is positive, customers are spending on board and bookings are booming. Overall, it looks extremely promising for Carnival Cruise.

Scale is another critical opportunity for Carnival Cruise. The company is the largest cruise line in the world. Carnival Corporation held a dominant position before the pandemic with passenger and revenue market shares at 47.4% and 39.4%, according to the NIH. This allows the company to operate worldwide and capitalize on growing demand and profitable markets. This also means that once the industry is completely online, it will have a significant advantage as the company has a massive fleet.

Another advantage of buying shares in Carnival Cruise is if you are a customer of the cruise company. The company offers attractive benefits to shareholders and is a significant opportunity for customers who tend to use their services. Customers who own shares in Carnival receive $50-$250 in onboard credits. You should hold 100 shares, which are worth ~$1000 at the current price. It means that even one cruise a year will return you 5%-25% of your investment. It is profitable if you are a sailing lover and gives you a significant incentive to invest.

The Risks

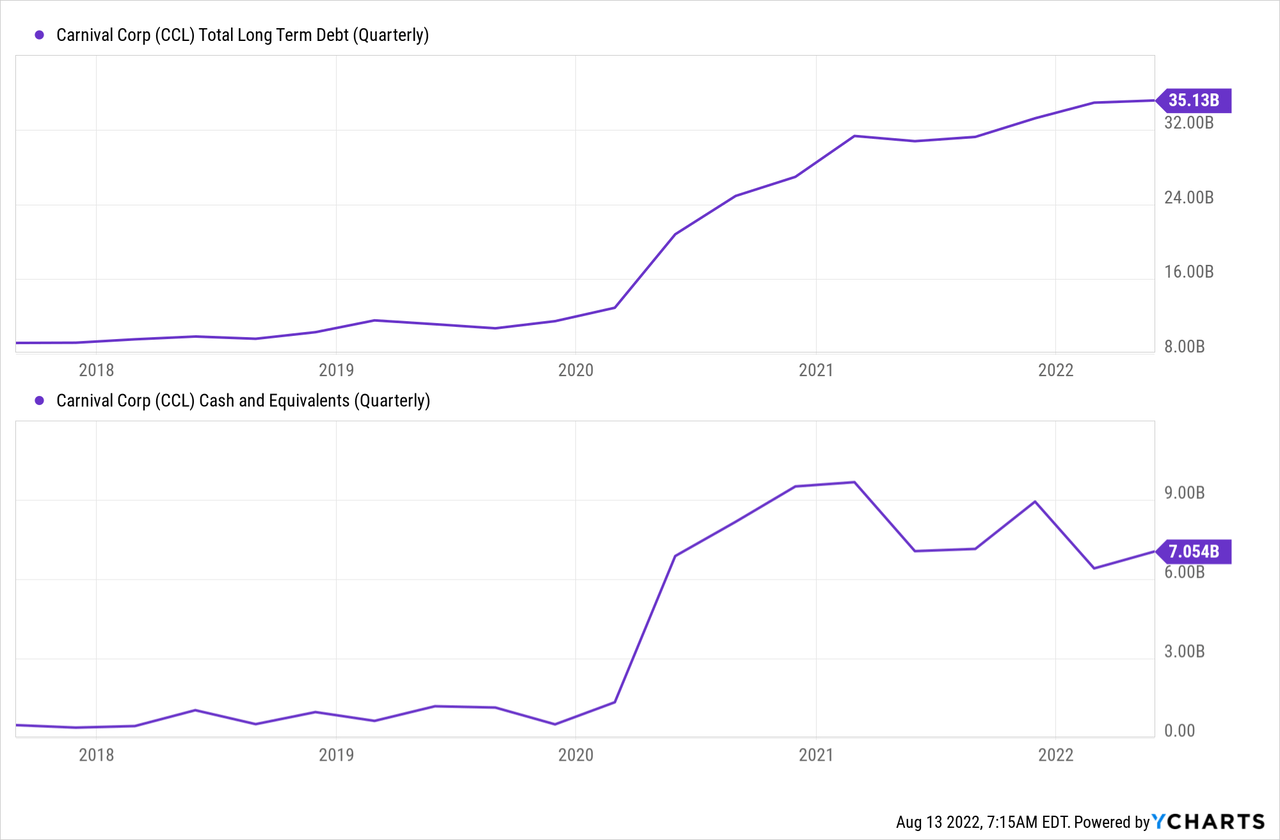

The first risk for the company is its debt level which has almost tripled since the start of the pandemic in 2020. The company will need to stabilize its balance sheet before paying a dividend, and it will have to this to regain its investment grade credit rating and get its operations up and running. Debt will weigh on its operations as interest rates rise, requiring more free cash flow. The company also has more cash and cash equivalents than before the pandemic. It is likely to use some to reduce the level of debt.

Another risk for the company is inflation. Inflation affects carnival sailing mainly due to higher fuel prices and labor costs. She also has to pay more for food and other materials, but fuel and labor are the most important. It’s challenging for a cruise line, as companies sell tickets in advance, and with an inflationary environment, it’s harder to price the product.

Another risk for Carnival Cruise is the risk of the current recession. The company’s recovery relies heavily on people returning to everyday life. It means limited unemployment and high spending. An ongoing recession means consumers may curtail discretionary spending significantly as they prepare for the impact. It will have a significant negative effect on the rate at which Carnival Cruise is recovering.

conclusions

Recovery is now a very credible option as we see booking leading to sales leading to cash from operations. This will eventually lead to the return of the benefit next year. The current valuation makes it attractive to invest in Carnival Cruise, however the current risks remind us that while there is significant upside, there is also significant downside. It’s a high-risk, high-reward game.

Investors with a high risk appetite can consider buying the stock now and hopefully enjoy all the upside while dealing with the risks associated with uncertainty. Investors with a lower risk appetite may wait until the company starts a dividend once again, showing high confidence that the situation is sustainable. The company is a risky BUY, in my opinion, as long as investors consider the risk.