Editorial SeregaSibTravel/iStock via Getty Images

The only piece of the puzzle that Carnival Corp. holds. (NYSE: CCL) and the cruise line sector returning from a full recovery were some of the ongoing restrictions on Covid. The sector received extremely good news from some very restrictive areas on Monday. My investment thesis remains ultra bullish on the stock due to a more than full recovery in the sector going forward, while the stock trades off recent lows.

Covid restrictions are disappearing

My recent research discussed how lifting certain restrictions on Covid in the US, such as the requirement for a vaccine, helped increase bookings. The industry received more good news on Monday as two of the most restrictive areas in China and Canada moved forward with lifting travel restrictions.

The biggest news was probably Canada. The restrictive country announced the lifting of all Covid travel restrictions effective October 1.

Travelers will no longer be required to submit public health information through a government app or website, provide proof of vaccination, undergo pre- or post-arrival testing, or quarantine or self-isolate. This declaration should fully open up cruise travel to Canada and even makes the restrictions in Canada less onerous than a US cruise that still requires a negative test for unvaccinated passengers.

At the same time, regulators signaled an e-visa for mainland Chinese travelers and tour groups to visit the gambling hub. The news is a good sign that China can finally reopen to global travel without restrictions.

Beyond some travel restrictions in Eastern Europe due to the war in Ukraine, the global cruise industry is getting closer and closer to normal. Carnivals were already surpassing 2019 booking levels with the latest trends.

Carnival has already jumped on board in Canada with Princess Cruises announcing the reopening of Princess Alaska cruises with Canada as a featured destination. The cruise line is choosing the right time to bring new ships on board.

Past 2019 cruise

The stock is struggling below $10, but CFO David Bernstein has discussed the potential to exceed 2019 EBITDA levels in 2023. The CFO made this statement on the FQ2’22 earnings call ahead of the recent uptick in bookings from the lifting of Covid restrictions:

I said so many times. I think we’re — what I’ve always said is that we have the potential for EBITDA to be greater in 2023 than in 2019. That’s a big characteristic, of course, is the price of fuel which has gone up quite a bit in the last few months. .

Adjusted EBITDA strips out interest expense, so of course the earnings picture doesn’t necessarily improve due to higher debt levels and rising interest rates. However, cruise ship stocks have essentially been left for dead or bankrupt, yet companies are predicting 2023 levels to reach previous levels.

Analysts expect FY22 revenue of $22.0 billion and FY23 revenue of $24.1 billion. FY19 peak revenue was a record $20.8 billion, up from just $18.9 billion a year earlier.

Investors should let these numbers sink in when the FY24 earnings target is for revenue to grow $3.2 billion over previous record numbers. Carnivals obviously face higher expenses due to inflation and high fuel prices along with hitting interest expenses.

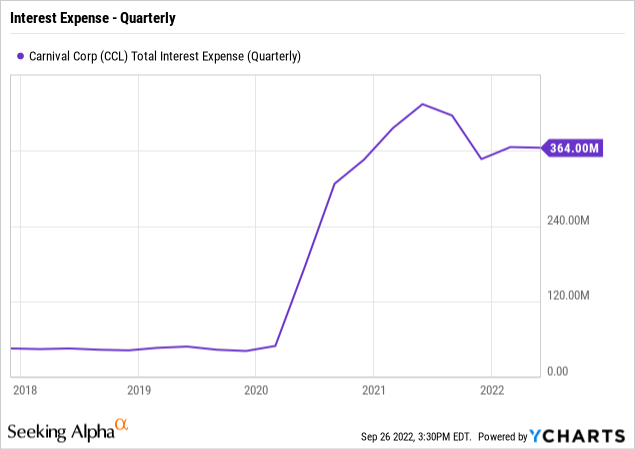

Interest expense was running at a quarterly rate of $50 million in FY19 and the expense has grown to over $360 million now. The difference is remarkable, but Carnival had expectations of generating $5.5 billion in annual cash flow from operations in FY20 before Covid hit.

Even a $1.2 billion increase in interest expense could be absorbed with those cash flows, especially on a much higher revenue base. The company is unencumbered by higher debt issues with a big push to expand capacity with capital spending not slowing until 2024 and 2025.

Source: Carnival FQ2’22 business update

The big key to the future results of FQ3 will be the discussions that return to normalized cash flows in FY23. Cruise lines are shedding all the Covid restrictions that left financial results uncertain. Carnival can now count on higher bookings and have much more confidence in future numbers.

The stock is trading extremely low at just $9 when all the uncertainty is leaving the sector. PE falls on 6x FY24 EPS targets of $1.52, but that number rose above $2.50 earlier in the year.

Some of the slow lifting of Covid restrictions pushed the recovery from FY22 to FY23, but the numbers should now normalize to the point where the only unknown is the interest rate impact if Carnival can further reduce interest expenses to boost earnings and cash flows.

Earlier estimates were for the cruise line to return to full earnings power of $2.50 to $3.00 when additional interest expense is stripped out.

Takeaway

The main thing for investors is that Carnival is very cheap here. The stock is priced for bankruptcy, yet the cruise line is returning record revenues that lead to strong cash flows and profits.